J#35: This stock is on sale: 20% off with strong Dividend Returns on the horizon

One of the best times to buy shares for the long run is when other investors succumb to emotional knee-jerk reactions to short-term news. For example, sometimes share prices slide when new policies are announced that seem to threaten a company’s operating landscape. For me, these are cues to scrutinize and uncover strategies that pave the way for healthy dividend returns.

Let’s zoom in on the recent share price slide of Eastern Company SAE (EC) from 15 Egyptian pounds in late February to 11.90 as of the 8th of April. This represents a fall of 20.6%. Based on prior year dividends, the current price of 11.90 provides a net trailing yield of 10.8% (12.1% gross, before a withholding tax rate of 10%).

What caused this sudden change in market sentiment?

The share price drop commenced in February 2021. The catalyst for the fall in share price was EC’s announcement that they were selling their Treasury Shares. Some 2.3% of company’s shares were repurchased by the company at the start of the COVID-19 pandemic (‘treasury shares’). These purchases were mandated by the Egyptian government to support EC’s price when markets collapsed in the initial stages of the pandemic.

The Company’s Board of Directors announced in February that they are selling the company’s treasury holdings. Company announcements were made (of both quantity and timing of the sale) and this resulted in downward selling price pressure, as some other investors decided to pre-empt the selling and get out first. In stock market parlance, the announcement had created a potential “overhang.” Shorter-term investors didn’t like that.

Then, on or about 21 March, an official announcement by the Egyptian government that a new cigarette manufacturing license (only one sole license will be issued regardless of number of bidders) would be up for sale and this could potentially terminate EC’s status as the monopolistic supplier of cigarettes in Egypt. This has kept EC’s share price at their current lower levels, some 20% below the February highs.

For more details, please refer to: Egypt introduces new license to produce cigarettes, Eastern Company comments

In my previous journals, I recommended EC as a BUY. The reasons were presented in:

J#26 – Targeting High Dividend Yields in Tobacco Companies

J#28 – How we Measure Potential Investment Returns of our Tobacco Companies

I remain a BUYER of Eastern Company SAE (EC) at the current price level for the following reasons:

- The company that acquires the new license (‘NewCo’) is required to have EC as a 24% shareholder. Moreover, EC does not have to pay any share of the cost of the license.

- NewCo would not have the right to produce cigarettes in the same cigarettes price category controlled and manufactured by Eastern Company, which represents 98% of its total revenues. This will guarantee that there is no real competitive threat for Eastern Company’s main products.

- No additional licenses will be offered for 10 years from the date of granting this new license.

- It is likely to take 24 months for NewCo to build a new cigarette-making plant. EC can therefore expect to continue to book the same level of revenue and profits regardless of the winning bidder for the next 1 to 2 years.

Based on the above, it is clear to me that EC will easily maintain its status as the dominant cigarette producer in Egypt for a very long time to come. Sure, a new player in the market would likely have an impact on EC’s sales volumes, but EC has strong government backing, as evidenced by the terms that NewCo is required to adhere to.

EC’s management response to the bidding announcement can be read here. They too seem unperturbed about the new license requirements.

Bidders were required to submit their offer by the end of April but this deadline was postponed indefinitely at the request of the bidders (refer to https://www.reuters.com/article/us-egypt-tobacco-idUSKBN2BR062).

I anticipate that the winning bidder may be one of the following international players:

- British American Tobacco

- Japan Tobacco

- Philip Morris International (PMI)

No one knows who will get, or even if any new cigarette manufacturing license will be given out. So, at this stage I believe it is premature to speculate as to what the industry impact may be. One possible future risk is that one of the companies for which EC currently does contract manufacturing in Egypt wins a license of its own, which means EC could lose part of its of contract manufacturing business, in addition to facing direct competition. But, with the Egyptian government as the majority shareholder in EC we are very confident that it will not shoot itself in the foot, by undermining EC’s competitive position or destroying a significant part of its business. The risk is overblown.

I continue to be well satisfied with EC’s Key Executive Team and their Prompt and Transparent answers to my Queries

On 22 March 2021, I attended a conference call with the management of EC — CEO, Hany Aman, and CFO, Mostafa Ahmed El Mahdi — to go over EC’s 2nd quarter 2020/2021 (quarter ended 31 December 2020) financial results.

Whilst the number of participants were not disclosed, I suspect there were fewer than 10 participants. My questions to the CEO on government cigarette duties and operating margins were given ‘air’ time. The low number of attendees is just what I like — with little attention given by mainstream financial markets analysts and investors, Egypt offers value.

The CEO’s answers were to the point. He had a grasp of the facts and stressed that EC’s policy is to reward its shareholders with dividends and that it is undisputedly an important company in Egypt’s growth (it aids government revenues through the smoking excise duties it collects and dividends it pays).

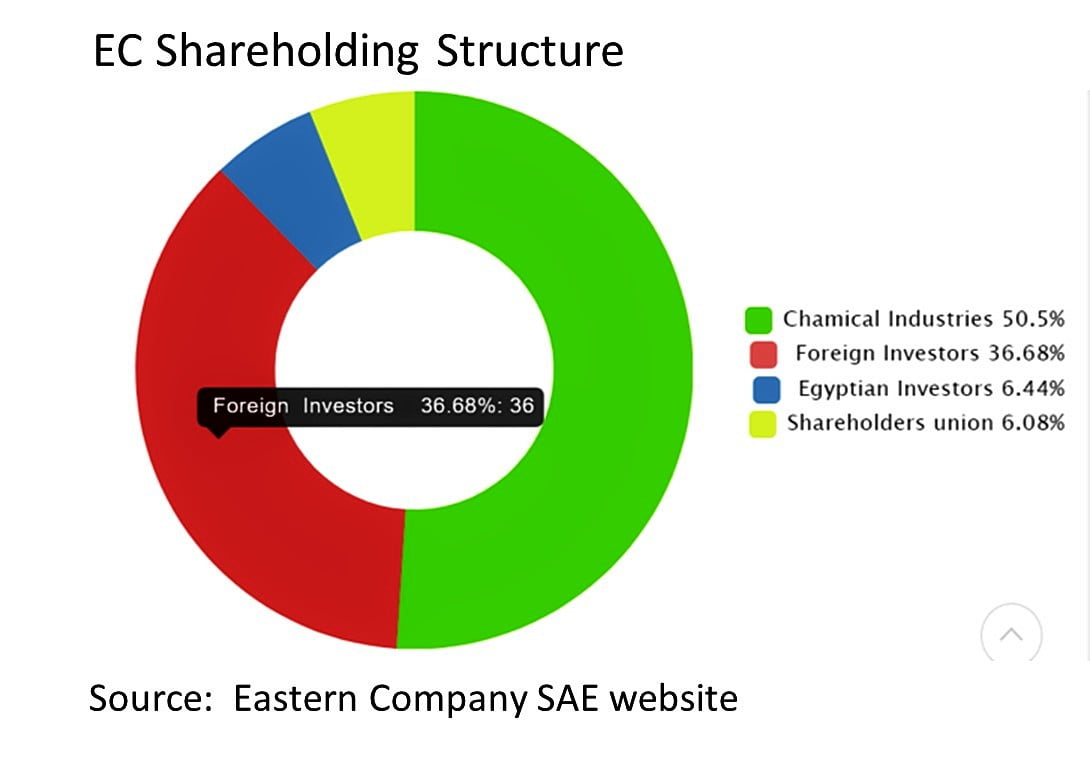

50.4% of EC is owned by Chemical Industries, a state-owned company. It is no wonder that despite announcing a new cigarette manufacturing license, the Egyptian government is protective of the industry and EC’s leading role in it.

2020/2021 is Shaping up to be a Stellar Year for Strong Dividends!

Extracts from notes taken during my meeting with management and my thoughts are presented below:

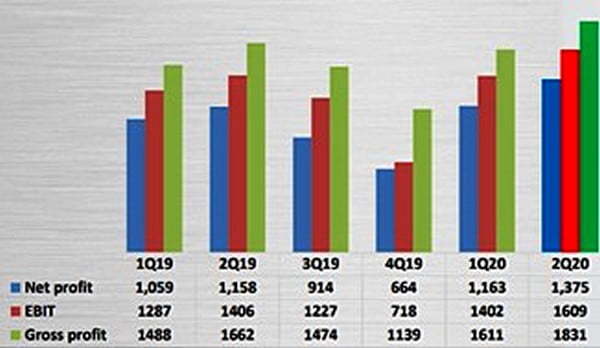

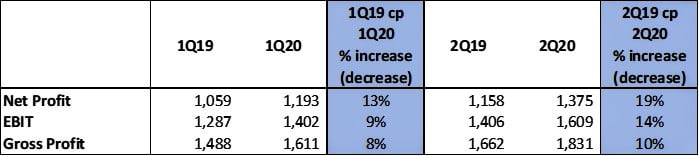

- Net Profit, EBIT and Gross Profit are seeing quarterly and year-on-year increases.

- On a year-by-year basis, Net Profit, Earnings Before Interest and Tax (EBIT) and Gross Profit increased between 8% and 19% (see table below).

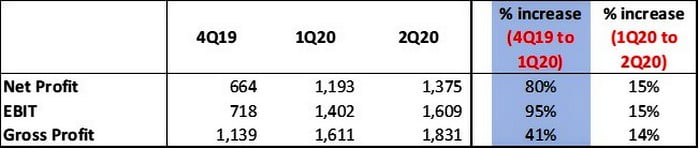

On a sequential quarterly basis, Net Profit, EBIT and Gross Profit increased by 14% to 15% (see table below) in the three months ended 31 December 2020.

The large 41% to 80% percentage gains in the prior quarter were as a result of supply chain disruptions from COVID in the quarter ended June 2020, and can be largely ignored as one-offs.

Note: EC has a financial reporting year-end of 30 June and their reporting format is to state their quarterly periods from the beginning of the financial year. Hence the current financial year’s (2020/2021) quarters are reported as:

- 1Q20 (ended Sep 30 2020),

- 2Q20 (ended Dec 31 2020)

- 3Q20 (ended Mar 31 2021)

- 4Q20 (ends Jun 30 2021)

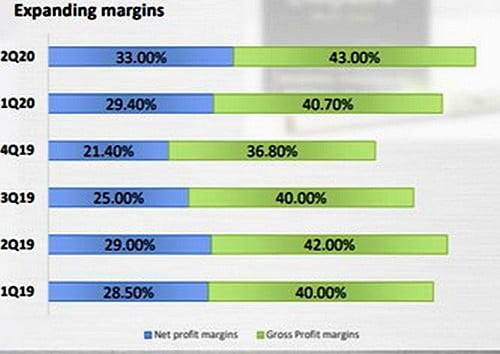

- Gross Profit increases were due to:

- An increase in consumption of EC’s higher-margin local brands (foreign brands are stable / declining).

- EC’s focus on improving cigarette distribution channels (the main reason for increasing consumption / sales).

- The COVID-19 pandemic has been a ‘plus’ for smoking volumes after supply chain disruptions during March to June 2020 were resolved.

- Cost management and cash management have been the major contributors to the margin increases. EC is less dependent on price increases of their product as, according to the CEO, they are mindful of the potential to adversely impact demand.

Gains from financial investments of surplus cash further boosting the bottom line

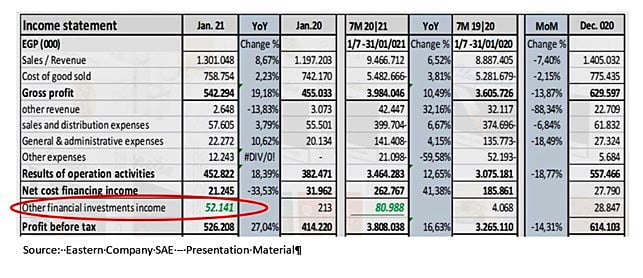

- NET Profit has been helped tremendously by the introduction of and focus on the company’s cash management. The company’s strategic cash management activities with the National Bank of Egypt saw surplus daily cash invested in T bonds and Eurobonds. For example, for the month of January, 10% of Profit before Tax (EGP 526.208) was derived from improved cash management activities (EGP 52.141).

- Management is reviewing what to do with EC’s land bank and improving/obtaining a yield from these assets. This is another potential source of income. However, it’s too early to tell how material this would be in increasing net profits.

- The company repurchased 2.3% of the outstanding shares at the start of the COVID-19 pandemic to support the company’s price when markets worldwide sold off sharply. The Company’s Board of Directors has since decided to sell these ‘treasury shares’ and the resulting gains, consistent with EC’s dividend policy to reward shareholders, are to be distributed as a dividend. A copy of EC’s announcement of the sale can be read here.

- My analysis of the treasury stock sale is that it would NOT result in a material gain to the dividends we would receive. Specifically, at a sale price of EGP 13.98 (period in which sales were occurring, compared to the current price of EGP 11.90), would add a relatively insignificant EGP0.03 in dividends per share. That is small when you consider the prior year’s total dividends of EGP1.43 per share.

Eastern Company SAE can be purchased using EFG Hermes as a broker.

It has been busy period for me. Amongst the many tasks of setting up the Fund is the setting up its brokerage account. As you are aware, I have elected to use EFG Hermes as one of my primary brokers.

Should you wish to open an account with them, kindly contact:

Ms. Norhan ElKhatib

Interest Claims and Account Opening Officer | Brokerage

Email: EFGHermes_NewAccounts@EFG-HERMES.com

Mention my name (and Double Digit Dividends Fund) and Norhan will assist you.

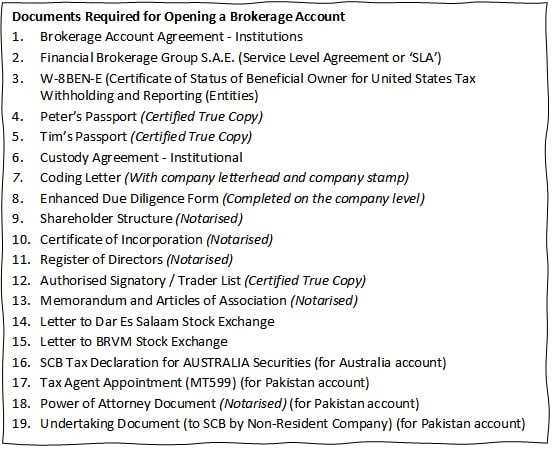

But I must warn you; like all account opening processes, it is complicated and time consuming. A list of the documents required for the Fund is provided below. It has required me to have 8 documents notarised and some additional 11 supporting documents. It is probably a more complicated task for me as I am opening an account for a company, rather than an individual, together with various custodian accounts.

I am presently also researching other brokers to ensure that the Fund is able to invest in markets that are not covered by EFG Hermes.

Finding quality double-digit yielding gems is hard work. Not only do you need to find them, you also need to be able to buy them! That is one of the advantages of subscribing to a Fund such as Double Digit Dividends – the account opening paperwork you require from us is kept to a minimum and we do the investing for you globally.

Not to scare you, but to give you an idea of the documents I had to prepare, here’s my list: