J#11: Boosting your investment results with the right exit strategy

There are times when you have to sell an investment that you have a strong emotional attachment to. This can be a difficult process as your emotions can cloud your selling decisions. Some examples include:

- You wish to hold on to an investment because of the great returns it has provided you in the past but which in reality are no longer there, even though you wish for those returns to happen again.

- The pain from closing your losing position makes you decide to hold on to the asset a little bit longer.

- The regret of not realizing gains when the opportunity was there for the taking makes you hold the investment even longer with the hope that those gains will reoccur.

- The fond memories it brings back to you through using a physical asset such as a car or a home.

There are five lessons I learnt from my triple-bagger shophouse investment experience (see Journal 7) — the 5th lesson was to always remember it is God’s money.

“God’s money” is a term I generally use to convey a mindset that your emotions should not dictate your investment decision on when to sell. To help you have this mindset, a pre-planned, well thought-out and systematically designed exit strategy for each and every investment you make is required. This exit strategy should be applied in both cases where the investment works out as planned (i.e. you make a profit), and where it does not (i.e. you make a loss).

By having a pre-planned and systematically designed exit strategy, you can be emotionally detached from the money involved. Selling becomes simply an application of your pre-designed strategy. All great investors do this. You are mentally focussed on applying your strategy, rather than being held back by the monetary gains or losses the investment has generated for you.

To illustrate, consider my shophouse investment and some of my stock investments.

My shophouse has been a great investment. It brings back happy memories of living there, and reminds me of the time, effort and love I spent building and maintaining that investment. Because of my divorce, it is likely that the shophouse will have to be sold. The full circle for this investment will then be complete.

The shophouse was originally bought to be an asset held by our family forever. THAT was the strategy. Yes, I would love to keep the shophouse but my personal circumstances have changed and it is important for me, as an investor, to be emotionally detached from the decision to sell the shophouse.

Selling the shophouse is hard to do. Nevertheless, as my late father would have said to me, it is important to “not be possessed by your possessions,” it is “God’s money.”

The same message is echoed in Rudyard Kipling’s famous poem “IF” where he wrote, “If you can meet with Triumph and Disaster and treat those two impostors just the same.”

In other words, whether the investment works out, or it doesn’t, you need a pre-determined exit strategy for each.

For our Double Digit Dividends investments, we also need to think about pre-determined exit strategies to ensure our emotions do not dictate the process. All good investors do this and it leads me to the topic of whether we deploy a hard or trailing stop loss to our Double Digit Dividend recommendations.

Stop Losses & Our Portfolio’s Exit Strategy

If you are new to the investment field, a “hard” stop loss is a percentage below our entry price where, should the market price fall below it, we immediately sell our entire position. A “trailing” stop loss is when you reset your exit price level continually based on a percentage of the highest price attained while you are invested. If the price pulls back by the percentage you set from the highest price reached during the time you have owned it, you sell your investment and realise any gains/losses. Both types of stop losses, theoretically, would limit any potential loss beyond that amount.

These are good strategies to minimise losses but are not appropriate for us. With our Double Digit Dividends stocks, we are not going to set a hard stop loss nor a trailing stop loss.

Our exit strategy must be based on the main reason we make these investments in the first place, that is, dividends. In the event the company materially cuts its DIVIDEND, THAT’S our trigger for an exit.

Now, that does not mean we will immediately sell every stock that cuts its dividend. Businesses are cyclical. Some of our holdings will have years where they cut the dividend modestly, or maybe even materially. But if it is the result of temporary cyclical factors, we shall continue to hold so long as the business fundamentals remain intact.

It is only where we conclude there has been a structural change to lower, or NO dividends, for some unforeseen reason, that we will see our “stop loss” and exit strategy being applied.

We adopt this approach as our investments are designed to be bought and held indefinitely, or until such time as our dividend investment thesis fails to apply. The market may, from time to time, change the company’s share price for whatever reason (and in some instances without any rationale). This may result in an unrealized capital loss or gain. If the company we are invested in maintains a strong balance sheet, a healthy operating margin, and continues to pay out dividends, why should we sell? Nothing has changed except for the company’s price as reflected by Mr. Market being pulled by those damn Wild Horses.

Regardless of market price movements, we remain emotionally detached from our unrealized gains and losses. Our pre-defined exit strategy is that we only sell when our dividend investment thesis fails.

The exception to this rule is when our recommendation has appreciated significantly, and the valuation has become stretched in our view. When this occurs, we may sell part or all of our position so as to find an alternative investment of similar quality, but which is trading at a much lower valuation. This maximises our potential to make money.

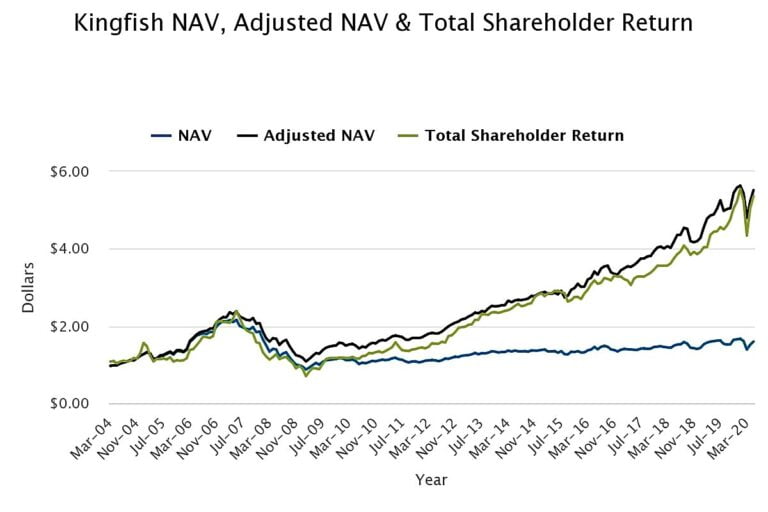

A good case in point is my recent sale of Kingfish Limited. Kingfish Limited is listed on the New Zealand Exchange. It was another investment gem. It had a double-digit yield, and a rock-solid balance sheet. I purchased it in early 2017 for NZD1.26 and sold it in November 2019 for NZD1.56.

I bought shares in May 2017 for NZD1.26

Sold them in two years for NZD1.56

Along the way I collected healthy double-digit dividends and more. Kingfish has a stated policy (unless it has changed) to pay out 2% of its net tangible asset (NTA) value each quarter (implying an 8% distribution yield if the stock were trading at NTA). When I first bought it, the stock was trading at a DISCOUNT to NTA. So, the yield was correspondingly higher. When the discount to NTA closed, the distribution yield became 8%. But, as the NTA had also appreciated significantly in that time period, I had a double source of capital appreciation and hefty gains. Moreover, free bonus warrants were issued that have a strike price which reduces by the amount of distributions made in the period up to the conversion date. I was, therefore, able to retain a cheap, leveraged exposure to Kingfish’s continued success.

I kept the warrants and exited my stock position as I felt my capital could be better redeployed from Kingfish shares into something with a higher yield, such as Twiga Cement. The sell trigger was Kingfish’s valuation – its discount to net tangible assets had substantially narrowed. Even though I was still booking a double-digit dividend, I took profits on the capital appreciation.

Not all my investments are winners. I am not perfect and I know of no investment manager who is. If an investment manager claims he has a 100% success rate, he or she must be selling you snake oil. There will be occasional losses at Double Digit Dividends.

For example, I used to own shares in a solid Lebanese bank, Blom Bank. It ticked all the boxes in my Double Digit Dividends selection criteria (i.e. a solid balance sheet, a history of double-digit dividend payments, a great balance sheet, and a well-run business with a wide operating margin). What changed was the macroeconomic picture of Lebanon. Lebanon defaulted on its sovereign debt and the Lebanese economy and Lebanese pound dropped like a stone. This resulted in Blom Bank’s price falling. I had to close my position and took a material loss. The investment thesis and evaluation were correct at a micro level. What I did not foresee was the speed of Lebanon’s economic and political implosion. I thought it had been sufficiently discounted, but it went from bad to worse. It is an interesting story of a Central bank telling lies and fudging their books. Refer to https://www.aljazeera.com/ajimpact/lebanon-central-bank-chief-inflated-assets-6bn-2018-200723163349241.html

The extent of any investment loss from a Double Digit Dividends investment will not be limited by setting a stop loss. It will be dictated by the time it takes us to come to the conclusion that the original investment thesis is truly broken. Conversely, by applying the same “when to sell” process based purely on whether our investment thesis is broken, it may result in Double Digit Dividends realising a gain before the market prices turn southward.

To reiterate, no Fund Manager has a 100% track record of success. At the end of the day what is important is we stick to a well-defined investment process with God’s money in mind. Needless to say, I shall try my best to ensure that more money is made than lost, all the more so, as my own money is at stake (see mandate).

Our Investment Process

As my business partner, Tim Staermose, wrote in his Global Value Hunter publication – “If you don’t have an investment process, you’re rudderless on the market sea.”

As most of my members know, I am a subscriber (see Journal #1) to the belief that it is vital to write your thought processes and observations down. If you cannot write it down, you don’t expose the shortcomings in your thinking process. Our investment process, which includes a pre-defined exit strategy needs to be codified in writing to ensure it is a sound process, and to use a metaphor, enables you to “stick to your knitting.”

In the journals ahead I shall share my thoughts on what to buy, when to buy, how much to buy and when to sell. This may also form part of the Investment Mandate should we decide to launch a Double Digit Dividend income fund.

A Message for My Children

Your Dad would love to discuss with you Kipling’s “IF” poem and how it relates to Plato’s analogy of wild horses. Can you work out what are some of the similarities (and differences) in their thinking?